Okay, let’s talk about something that could seriously change how we handle money – especially if you’re someone who deals with international transactions or dreams of easier travel in Europe. The Reserve Bank of India (RBI) just dropped a bit of a bomb: they’re planning to link India’s UPI TIPS Interlinking with the EU’s TIPS (TARGET Instant Payment Settlement) system. At first glance, it might seem like just another financial announcement, right? But trust me, this is bigger than it sounds. This isn’t just about convenience; it’s about reshaping the financial landscape for Indians.

Why This Matters | The Big Picture

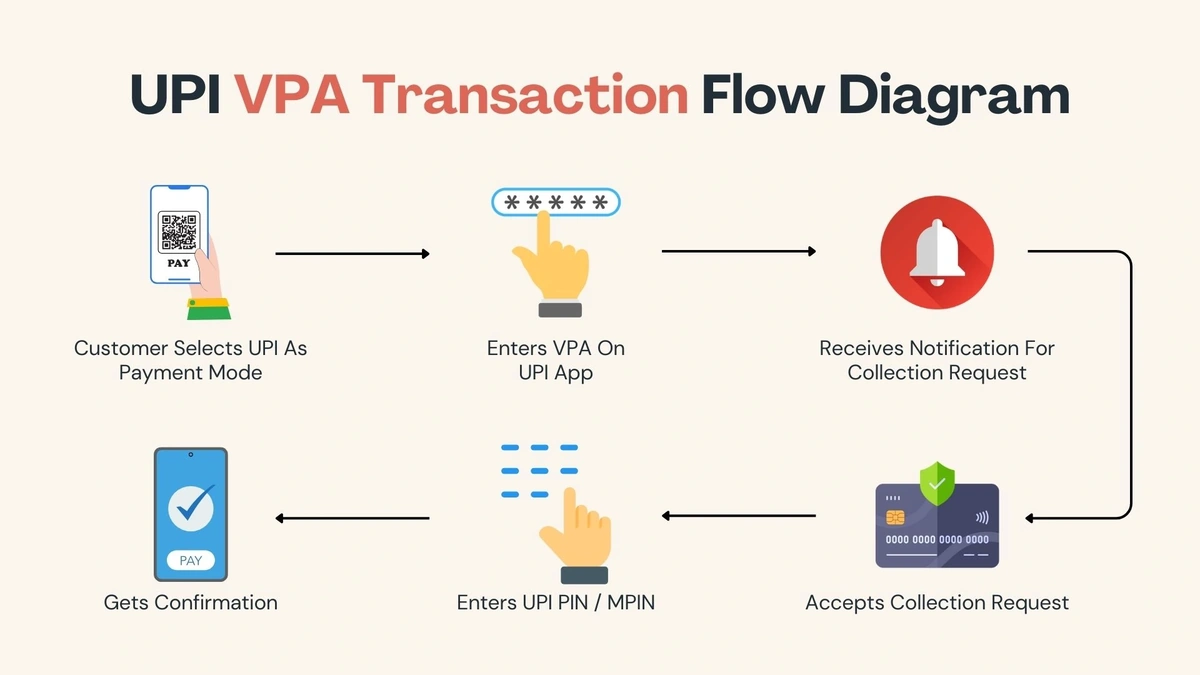

So, why is everyone buzzing about this UPI and TIPS Integration ? Well, consider this: currently, cross-border transactions can be a pain. You’ve got exchange rates, hefty fees, and the whole waiting game. This initiative aims to make instant, cheaper payments a reality between India and Europe. What fascinates me is the potential for boosting trade and tourism. Imagine Indian businesses easily receiving payments from European clients, or tourists paying for their gelato in Rome directly through their UPI app. This move could reduce our reliance on intermediaries and could lower the overall transaction cost.

Think about it – the current system often involves multiple banks and correspondent banking relationships, each adding their fees and delays. By linking UPI with TIPS, we are potentially cutting out several layers of complexity. This is a significant step towards financial inclusion, making international transactions accessible to small businesses and individuals alike. The beauty of UPI (Unified Payments Interface) lies in its simplicity and widespread adoption in India. Linking it with TIPS could introduce a new level of convenience.UPIhas revolutionized how we make payments here, and now it’s set to make waves internationally.

How Will It Actually Work?

Now, let’s get into the nitty-gritty. How will the UPI and EU Payment Systems Connection actually work? While the exact details are still being ironed out, the basic idea involves creating a bridge between the two systems. This would likely involve setting up a mechanism for real-time currency conversion and ensuring compliance with regulatory requirements in both regions. According to various reports, the initial focus will be on facilitating payments for specific use cases, such as tourism and education. Over time, this could be expanded to include a broader range of transactions.

The one thing to remember here: security is paramount. Any linkage between payment systems must adhere to stringent security standards to prevent fraud and data breaches. It will be crucial to have robust authentication mechanisms and encryption protocols in place. And frankly, ensuring interoperability isn’t just a technological challenge. It also requires close collaboration between regulatory bodies in India and the EU to address legal and compliance issues. A common mistake I see people make is assuming it’s just a tech problem. It’s about policy, trust, and making sure everyone plays by the same rules.

Potential Benefits for You and Me

Okay, let’s get down to brass tacks. What’s in it for you and me? Well, imagine you’re planning a trip to Europe. Instead of dealing with currency exchange and carrying cash, you could simply use your UPI app to pay for your hotel, meals, and souvenirs. Or, if you’re an Indian business exporting goods to Europe, you can receive payments directly into your bank account without the hassle of dealing with intermediaries. This RBI initiative has the potential to significantly reduce transaction costs and settlement times, making international trade more accessible for small and medium-sized enterprises (SMEs).

Consider the implications for freelancers and remote workers. Many Indians work for European companies and face challenges in receiving payments. This linkage could simplify the process, allowing them to receive payments quickly and at a lower cost. And what I want to emphasize here, is the potential for boosting financial inclusion. It makes international transactions more accessible to everyone, regardless of their income level. By reducing the cost and complexity of cross-border payments, we are leveling the playing field and creating new opportunities for economic growth.

Challenges and Roadblocks

Now, before we get too carried away, let’s talk about the potential roadblocks. Implementing this linkage won’t be a walk in the park. Several challenges need to be addressed. Ensuring seamless interoperability between UPI and TIPS is no easy task. The two systems have different technical architectures and operate under different regulatory frameworks. Addressing these differences requires technical expertise and close collaboration between the relevant stakeholders.

Another challenge is managing currency exchange rate fluctuations . The value of the rupee and the euro can fluctuate significantly, which could impact the cost of transactions. To mitigate this risk, a robust mechanism for real-time currency conversion is needed. Let me rephrase that for clarity – this isn’t just about connecting two systems; it’s about building trust and ensuring that everyone benefits from the arrangement. I initially thought this was straightforward, but then I realized it’s a multifaceted problem involving technology, policy, and human behavior.

Future Implications and What to Watch For

So, what does the future hold? If this UPI and TIPS experiment succeeds, it could pave the way for similar linkages with other payment systems around the world. This could lead to a truly global payment network, where individuals and businesses can transact seamlessly across borders. It is also crucial to learn the implications of digital payment integration for global trade. The possibilities are exciting, but let’s be honest, there’s a lot of work to be done.

Keep an eye out for further announcements from the RBI and the European Central Bank. They’ll likely provide more details on the implementation timeline and the specific use cases that will be supported. And frankly, pay close attention to the security measures that are put in place. Ensuring the safety and security of transactions is paramount. If successful, this UPI TIPS Interlinking could herald a new era of global payments, making international transactions as easy as paying for your morning chai.

Speaking of global aspirations, have you checked out the investment Groww has made in Lenskart? This could be a significant boost for the Indian market. You can read more about it at Groww vs Lenskart IPO .

FAQ Section

Frequently Asked Questions

What exactly is TIPS?

TIPS stands for TARGET Instant Payment Settlement. It’s the European Central Bank’s system for instant payments in euro.

How will this affect transaction fees?

The goal is to reduce transaction fees by cutting out intermediaries and streamlining the payment process.

When will this linkage be implemented?

The RBI has announced the plans, but the exact timeline for implementation is still to be determined. Keep an eye on official announcements.

Is my UPI data safe during these international transactions?

Security is a top priority. Robust authentication and encryption protocols will be implemented to protect your data.

Will this work for all European countries?

Initially, it will likely focus on countries within the EU that use the TIPS system. Further expansion may follow.

What if I face issues during a UPI transaction in Europe?

Standard UPI customer support channels will be available to assist with any issues you might encounter.

And, just in case you were curious about other global financial changes, here’s a related article: Anil Ambani Group Assets Seized .